Bank Lobby Threatens ‘Great Taking’ Author David Webb

David Webb, author of The Great Taking, just exposed how banks and their political allies have systematically removed your property rights over securities. You might think you own your investments, but legally, your broker does and if they collapse, you have no right to reclaim them.

Webb and G. Edward Griffin have been fighting to strike exemptions in Article 8 of the Uniform Commercial Code, which prioritizes secured creditors over individual investors. But every attempt has been crushed by the banking lobby, which floods state legislatures with money, influence, and outright lies.

State lawmakers are folding under pressure. Banks have rigged the system, and most Americans aren’t lifting a finger to stop it.

The message is clear: no one is coming to save you. If you don’t take action, the banks will own everything—including what you think is yours.

The walls are closing in on your financial freedom—but not in the way most Americans believe.

While the debate rages over the future threat of Central Bank Digital Currencies (CBDCs), a far more insidious reality has already taken hold: our existing financial system already functions as a digital control grid, monitoring transactions, restricting choices, and enforcing compliance through programmable money.

For over two years, my wife and I have traveled across 22 states warning about the rapid expansion of financial surveillance. What began as research into cryptocurrency crackdowns revealed something far more alarming: the United States already operates under what amounts to a CBDC.

92% of all US dollars exist only as entries in databases.

Your transactions are monitored by government agencies—without warrants.

Your access to money can be revoked at any time with a keystroke.

The Federal Reserve processes over $4 trillion daily through its Oracle database system, while commercial banks impose programmable restrictions on what you can buy and how you can spend your own money. The IRS, NSA, and Treasury Department collect and analyze financial data without meaningful oversight, weaponizing money as a tool of control. This isn’t speculation—it’s documented reality.

Now, as President Trump’s Executive Order 14178 ostensibly “bans” CBDCs, his administration is quietly advancing stablecoin legislation that would hand digital currency control to the same banking cartel that owns the Federal Reserve. The STABLE Act and GENIUS Act don’t protect financial privacy—they enshrine financial surveillance into law, requiring strict KYC tracking on every transaction.

This isn’t defeating digital tyranny—it’s rebranding it.

This article cuts through the distractions to expose a sobering truth: the battle isn’t about stopping a future CBDC—it’s about recognizing the financial surveillance system that already exists. Your financial sovereignty is already under attack, and the last off-ramps are disappearing.

The time for complacency has passed. The surveillance state isn’t coming—it’s here.

Understanding the Battlefield: Key Terms and Concepts

To fully grasp how deeply financial surveillance has already penetrated our lives, we must first understand the terminology being used—and often deliberately obscured—by government officials, central bankers, and financial institutions. The following key definitions will serve as a foundation for our discussion, cutting through the technical jargon to reveal the true nature of what’s at stake:

Before diving deeper into the financial surveillance system we face today, let’s establish clear definitions for the key concepts discussed throughout this article:

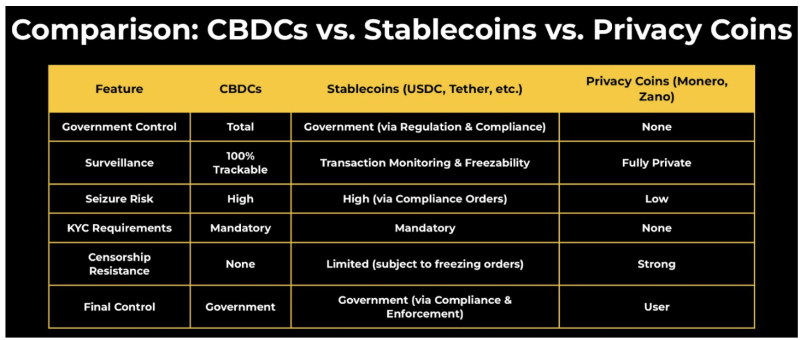

Central Bank Digital Currency (CBDC)

A digital form of central bank money, issued and controlled by a nation’s monetary authority. While often portrayed as a future innovation, I argue in “Fifty Shades of Central Bank Tyranny” that the US dollar already functions as a CBDC, with over 92% existing only as digital entries in Federal Reserve and commercial bank databases.

Stablecoin

A type of cryptocurrency designed to maintain a stable value by pegging to an external asset, typically the US dollar. Major examples include:

Tether (USDT): The largest stablecoin ($140 billion market cap), managed by Tether Limited with reserves held by Cantor Fitzgerald

USD Coin (USDC): Second-largest stablecoin ($25 billion market cap), issued by Circle Internet Financial with backing from Goldman Sachs and BlackRock

Bank-Issued Stablecoins: Stablecoins issued directly by major financial institutions like JPMorgan Chase (JPM Coin) or Bank of America, which function as digital dollars but remain under full regulatory control, allowing programmable restrictions and surveillance comparable to a CBDC.

Tokenization

The process of converting rights to an asset into a digital token on a blockchain or database. This applies to both currencies and other assets like real estate, stocks, or commodities. Tokenization enables:

Digital representation of ownership

Programmability (restrictions on how/when/where assets can be used)

Traceability of all transactions

Regulated Liability Network (RLN)

A proposed financial infrastructure that would connect central banks, commercial banks, and tokenized assets on a unified digital platform, enabling comprehensive tracking and potential control of all financial assets.

Privacy Coins

Cryptocurrencies specifically designed to preserve transaction privacy and resist surveillance:

Monero (XMR): Uses ring signatures, stealth addresses, and confidential transactions to conceal sender, receiver, and amount

Zano (ZANO): Offers enhanced privacy with Confidential Layer technology that can extend privacy features to other cryptocurrencies

Programmable Money

Currency that contains embedded rules controlling how, when, where, and by whom it can be used. Examples already exist in:

Health Savings Accounts (HSAs) that restrict purchases to approved medical expenses

The Doconomy Mastercard that tracks and limits spending based on carbon footprint

Electronic Benefit Transfer (EBT) cards that restrict purchases to approved food items

Know Your Customer (KYC) / Anti-Money Laundering (AML)

Regulatory frameworks require financial institutions to verify customer identities and report suspicious transactions. While ostensibly aimed at preventing crime, these regulations have expanded to create comprehensive financial surveillance with minimal oversight.

Bank Secrecy Act (BSA) / Patriot Act

US laws mandate financial surveillance, eliminate transaction privacy, and grant government agencies broad powers to monitor financial activity without warrants. These laws form the legislative foundation of the current financial control system.

STABLE Act / GENIUS Act

Proposed legislation would restrict stablecoin issuance to banks and regulated entities, requiring comprehensive KYC/AML compliance and effectively bringing stablecoins under the same surveillance framework as traditional banking.

Understanding these terms is essential for recognizing how our existing financial system already functions as a mechanism of digital control, despite the absence of an officially designated “CBDC.”

The Digital Dollar Reality: America’s Unacknowledged CBDC

The greatest sleight of hand in modern finance isn’t cryptocurrency or complex derivatives—it’s convincing Americans they don’t already live under a Central Bank Digital Currency system. Let’s dismantle this illusion by examining how our current dollar already functions as a fully operational CBDC.

The Digital Foundation of Today’s Dollar

When most Americans picture money, they imagine physical cash changing hands. Yet this mental image is profoundly outdated—92% of all US currency exists solely as digital entries in databases, with no physical form whatsoever. The Federal Reserve, our central bank, doesn’t create most new money by printing bills; it generates it by adding numbers to an Oracle database.

This process begins when the government sells Treasury securities (IOUs) to the Federal Reserve. Where does the Fed get money to buy these securities? It simply adds digits to its database—creating money from nothing. The government then pays its bills through its account at the Fed, transferring these digital dollars to vendors, employees, and benefit recipients.

The Fed’s digital infrastructure processes over $4 trillion in transactions daily, all without a single physical dollar changing hands. This isn’t some small experimental system—it’s the backbone of our entire economy.

The Banking Extension

Commercial banks extend this digital system. When you deposit money, the bank records it in their Microsoft or Oracle database. Through fractional reserve banking, they then create additional digital money—up to 9 times your deposit—to loan to others. This multiplication happens entirely in databases, with no new physical currency involved.

Until recently, banks were required to keep 10% of deposits as reserves at the Federal Reserve. Covid-19 legislation removed even this minimal requirement, though most banks still maintain similar levels for operational reasons. The key point remains: the dollar predominantly exists as entries in a network of databases controlled by the Fed and commercial banks.

Already Programmable, Already Tracked

Those who fear a future CBDC’s ability to program and restrict money use miss a crucial reality: our current digital dollars already have these capabilities built in.

Consider these existing examples:

Health Savings Accounts (HSAs): These accounts restrict spending to approved medical expenses through merchant category codes (MCCs) programmed into the payment system. Try to buy non-medical items with HSA funds, and the transaction is automatically declined.

The Doconomy Mastercard: This credit card, co-sponsored by the United Nations through its Climate Action SDG, tracks users’ carbon footprints from purchases and can shut off access when a predetermined carbon limit is reached.

Electronic Benefit Transfer (EBT) cards: Government assistance programs already use programmable restrictions to control what recipients can purchase, automatically declining transactions for unauthorized products.

These aren’t theoretical capabilities—they’re operational today, using the exact same digital dollar infrastructure we already have.

Surveillance and Censorship: Present, Not Future

The surveillance apparatus for our digital dollars is equally established. The Bank Secrecy Act mandates that financial institutions report “suspicious” transactions, while the Patriot Act expanded these monitoring requirements dramatically. The IRS uses artificial intelligence to scrutinize spending patterns across millions of accounts, while the NSA bulk collects financial data through programs revealed by Edward Snowden.

This surveillance enables active censorship, as demonstrated during Canada’s trucker protests in 2022, when banks froze accounts of donors without judicial review. Similar account freezes have targeted individuals ranging from Kanye West to Dr. Joseph Mercola—all using the existing digital dollar system.

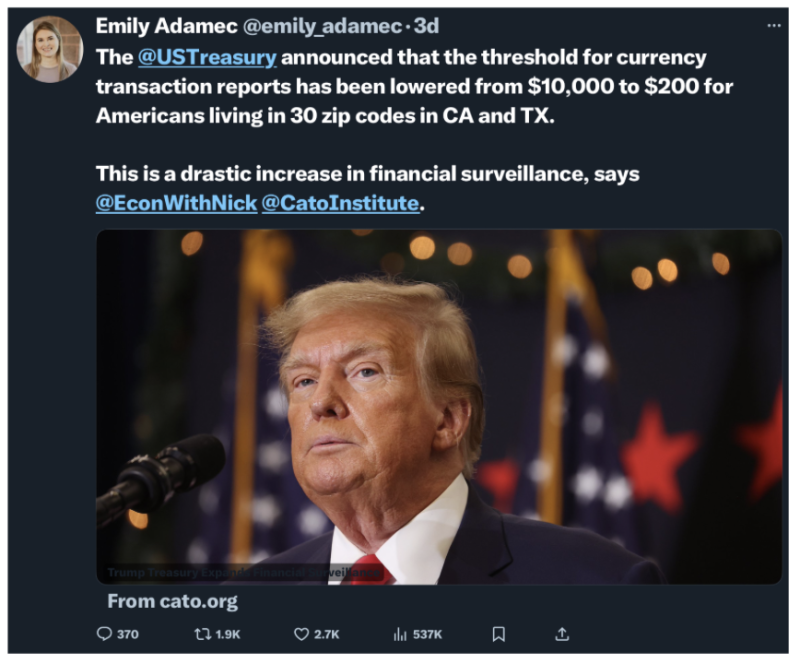

In March 2025, the Treasury intensified this framework, lowering the cash transaction reporting threshold from $10,000 to $200 across 30 ZIP codes near the southwest border, subjecting over a million Americans to heightened scrutiny under the guise of curbing illicit activity.

The Semantic Shell Game

When politicians and central bankers claim we don’t have a CBDC, they’re playing a game of definitions. The substantive elements that define a CBDC—digital creation, central bank issuance, programmability, surveillance, and censorship capability—are all present in our current system.

The debate over implementing a “new” CBDC is largely a distraction. We’re not discussing whether to create a digital dollar—we’re discussing whether to acknowledge the one we already have and how to modify its architecture to further enhance surveillance and control.

Understanding this reality is the first step toward recognizing that the battle for financial privacy and autonomy isn’t about stopping some future implementation—it’s about confronting and reforming a system already firmly in place.

The Weaponization of Financial Surveillance

The government justifies financial surveillance under the guise of fighting terrorism, money laundering, and organized crime, but the data tells a different story. Since the passage of the Bank Secrecy Act (BSA) in 1970 and the Patriot Act in 2001, the US government has accumulated trillions of financial records on ordinary Americans, yet these laws have failed to curb financial crime. Instead, they have been used to target political dissidents, seize assets without due process, and criminalize cash transactions.

The US Treasury admitted it cannot track $4.7 trillion in spending, yet demands compliance from individuals over transactions as small as $600.

The Financial Crimes Enforcement Network (FinCEN) has harvested billions of transaction records but has failed to demonstrate any meaningful reduction in financial crime.

Suspicious Activity Reports (SARs) are used to justify asset seizures without charges, while banks like JPMorgan and HSBC have laundered billions for drug cartels with no consequences.

The US Dollar remains the primary currency for terrorism, human trafficking, and war financing—yet the government wants to blame privacy coins.

These financial laws were never about stopping crime—they were about controlling the people. Meanwhile, the same government that demands total visibility over our money has lost track of trillions and even funneled taxpayer dollars directly to terrorist groups. If financial transparency is so important, perhaps the US Treasury should be the first to comply.

Defining the Real Threat: The Government’s Surveillance Machine

Before we delve deeper, let’s cut through the noise and define the true stakes—because the focus on banning a Central Bank Digital Currency (CBDC) and vilifying the Federal Reserve misses the bigger picture. President Trump and others have zeroed in on the Federal Reserve as the architect of digital tyranny, with a public blame game unfolding as the Fed, federal government, and commercial banks point fingers at each other like squabbling overlords.

But this distraction obscures the real enemy: a government surveillance apparatus that already tracks, programs, and censors our money, paving the way for digital tyranny—social credit systems, digital IDs, vaccine passports, and more. The Federal Reserve is just one cog; the government’s machinery, backed by the banks that own the Fed, is the true enforcer.

The End Goal: Digitizing Everything

My two-year crusade against Central Bank Digital Currencies (CBDCs) stems from a chilling realization: the endgame isn’t just controlling our money—it’s digitizing all our assets—money, stocks, bonds, real estate, and more—under a global ledger with the same tracking and programmability as CBDCs.

As I detail in my book The Final Countdown, this vision involves CBDCs paired with Regulated Liability Networks (RLNs), systems designed to tokenize every financial instrument—stocks, bonds, and beyond—settling only in CBDCs. Countries like the US, those in Europe, the UK, and Japan are developing their own RLNs, engineered to interoperate, creating a seamless global ledger. The ultimate aim, rooted in the technocracy movement since the 1930s, is a single digital currency backed by energy credits, tying our wealth to resource consumption and a social credit system.

This isn’t speculation—it’s a deliberate blueprint. RLNs enable central banks and governments to monitor and program every asset, ensuring compliance with policies like carbon limits or social scores. The technocracy movement, founded by figures like Howard Scott in the 1930s, envisioned energy as the basis of economic value, a concept now resurfacing in digital form. This global ledger threatens to erase ownership and freedom, a reality already taking shape as governments and banks tighten their grip. This sets the stage to uncover how the US government’s surveillance machine, already in motion, accelerates this dystopian future.

The Government’s Surveillance Arsenal

The US government has perfected financial surveillance long before any CBDC label was applied, as I detailed in my Brownstone Institute article “Fifty Shades of Central Bank Tyranny.” The National Security Agency (NSA) bulk collects financial data on domestic and international transactions, a revelation from Edward Snowden exposing its access to phone calls, internet communications, and undersea cable intercepts—turning your bank account into a government peephole.

The IRS, wielding artificial intelligence, scrutinizes spending patterns with chilling precision, as seen in Rebecca Brown’s 2015 case, where $91,800 was seized via civil asset forfeiture for no crime, or the IRS’s recent mandate forcing Venmo and PayPal to report transactions over $600, ensnaring even the smallest earners. These AI tools transform every purchase into a potential target for government scrutiny.

The Patriot Act amplifies this overreach, authorizing warrantless wiretapping and data collection, while National Security Letters (NSLs)—like the one silencing Nick Merrill in 2004, gagging him from consulting a lawyer about FBI demands—ensure silence under threat of law. The Bank Secrecy Act compels banks to report “suspicious” activity, fueling Operation Chokepoint 2.0, where commercial banks like JPMorgan Chase and Bank of America froze accounts of dissenters—Kanye West, Melania and Barron Trump, Dr. Joseph Mercola—often exceeding federal directives. Congress, not the Fed, drives this surveillance juggernaut, embedding it through bipartisan laws like the Patriot Act, Bank Secrecy Act, CARES Act, and the addition of 87,000 armed IRS agents poised to audit the average citizen.

A Distinction Without a Difference

Focusing solely on the Federal Reserve as the villain is a distinction without a difference. The Fed, a private entity veiled in secrecy, is owned by the largest commercial banks—JPMorgan Chase, Citibank, and others—forming a cartel that profits from the system, as G. Edward Griffin’s The Creature from Jekyll Island exposes. Its digital money creation feeds these banks, which multiply it through fractional reserves. Eliminating the Fed and letting the government issue currency directly, as Senator Ron Wyden advocates—a stance I challenged at a conference where he opposed CBDCs but endorsed government control—wouldn’t end surveillance; it would intensify it. Wyden’s vision centralizes power further, removing the Fed’s buffer and amplifying government oversight with no accountability.

The real threat lies in the system’s design: digital money is already tracked and censored by government decree. Whether it’s the Fed’s Oracle databases or banks’ Microsoft systems, the infrastructure is programmable, enabling control without new laws—just new rules, crafted daily in backrooms. This surveillance machine, not the Fed alone, drives us toward a dystopian future where every transaction fuels tyranny. With this system already entrenched in the US, the global race for CBDCs—and the US’s pivot to stablecoins under the STABLE and GENIUS Acts—only accelerates the spread of this control, amplifying the threat both abroad and at home. We must confront this escalating reality head-on to grasp the full scope of the battle for our financial freedom.

Global CBDC Development Accelerates Despite Trump’s Ban

Even with President Trump’s Executive Order (EO) 14178, signed on January 23, 2025, banning the Federal Reserve and other US agencies from pursuing a Central Bank Digital Currency (CBDC), the global race to develop CBDCs has not slowed down—it’s actually speeding up. Before the EO, 134 countries and currency unions, representing 98% of global GDP, were actively exploring CBDCs, according to the Atlantic Council’s Central Bank Digital Currency Tracker. With the US stepping back from explicit CBDC work, that number drops to 133 countries.

The US accounts for approximately 26% of global GDP (based on 2024 World Bank estimates of a $105 trillion global GDP, with the US contributing $27 trillion). Subtracting the US share, the remaining 133 countries still represent about 72% of global GDP—a massive portion of the world economy—continuing their CBDC efforts. Meanwhile, the US has shifted its focus to a backdoor approach through stablecoins, empowering commercial banks and the Federal Reserve to extend digital control at the expense of privacy and decentralized finance (DeFi).

The US pivot isn’t just about stablecoins like Tether and USDC—it’s a broader strategy codified in two legislative proposals: the STABLE Act (House, February 6, 2025) and the GENIUS Act (Senate, February 4, 2025). These bills restrict stablecoin issuance to insured depository institutions, federal nonbanks, and state-regulated entities, effectively handing the reins to big banks like JPMorgan Chase and the Federal Reserve’s network of member banks.

The STABLE Act bans unauthorized issuers, while the GENIUS Act prohibits unapproved payment stablecoins, ensuring only the financial elite can play. Both mandate strict Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements, turning every transaction into a surveillance opportunity. Algorithmic stablecoins used in DeFi platforms, which thrive on anonymity and decentralization, are effectively sidelined, as banks and the Fed tighten their grip on the digital dollar ecosystem. This isn’t innovation—it’s a power grab, cloaked as financial stability.

The pace of global CBDC development remains striking. In May 2020, only 35 countries were exploring CBDCs. By early 2025, that number had ballooned to 134 before the US exit, with 65 in advanced stages—development, pilot, or launch. Every G20 country except the US is now involved, with 19 in advanced stages and 13 running pilots, including Brazil, Japan, India, Australia, Russia, and Turkey. Three countries—the Bahamas, Jamaica, and Nigeria—have fully launched retail CBDCs, and 44 pilots are ongoing worldwide. This momentum persists despite Trump’s ban, as other nations see CBDCs as a way to modernize payments, enhance financial inclusion, and compete geopolitically, especially with China’s digital yuan (e-CNY) pilot, the largest globally, reaching 260 million people.

Recent developments underscore this acceleration. In Israel, the Bank of Israel released a 110-page design document in early March 2025, detailing plans for a Digital Shekel. This follows years of research and aligns with Israel’s participation in a 2022 project with the Bank for International Settlements to test international retail and remittance payments using CBDCs. The Digital Shekel aims to improve transaction efficiency and financial access across its tech-savvy population, marking a significant step toward implementation.

In the European Union, the European Central Bank (ECB) is pressing forward with its digital euro, targeting a rollout by October 2025. ECB President Christine Lagarde has been vocal about this timeline, stating in a recent address, “We are on track to introduce the digital euro by October this year, offering a secure and programmable complement to cash that ensures financial inclusion while maintaining privacy standards.” This follows the ECB’s October 2023 decision to enter the preparation phase for a digital retail euro, with a focus on both retail and wholesale applications. The EU’s push reflects a broader European trend, with countries like Sweden and the UK also advancing CBDC pilots, aiming to reduce reliance on US-dominated payment networks like Visa and Mastercard.

Across the Atlantic, Canada’s new Prime Minister, Mark Carney, who assumed office in March 2025, brings a pro-CBDC stance to the table. Carney, a former Governor of the Bank of England from 2013 to 2020, has long advocated for digital currencies as a tool for financial innovation. During his tenure at the Bank of England, he oversaw early CBDC research, including the July 2019 CBDC Technology Forum, which laid the groundwork for the digital pound.

Carney’s alignment with the World Economic Forum (WEF), where he has been a prominent figure pushing for sustainable finance and digital transformation, further underscores his support for CBDCs. The WEF has been a strong advocate for CBDCs, hosting roundtables through 2023 to promote interoperable designs. Under Carney’s leadership, Canada is likely to accelerate its CBDC efforts, building on the Bank of Canada’s 2023 analytical note emphasizing offline payment functionality—a move that could deepen digital control over Canadian finances.

Despite Trump’s EO, the global CBDC train is charging ahead, with the US taking a detour through stablecoins that empower banks and the Fed while stifling privacy and DeFi. The Digital Shekel, the EU’s October rollout, and Canada’s new leadership under Carney show that the world isn’t waiting for the US to catch up—it’s forging a digital future where control, not freedom, may be the ultimate prize.

Stablecoin Legislation: Backdoor CBDCs by Design

to read the rest of the artile, go to: https://brownstone.org/articles/the-stablecoin-trap-the-backdoor-to-total-financial-control/

A massive industry exists to prevent pandemics, but despite receiving billions each year, it routinely fails to prevent pandemics or provide viable ways to address those which emerge.

This industry rests upon the lie that viral diseases cannot be treated, when in reality there are many effective over-the-counter, and unpatentable treatments for viral illnesses.

The industry engages in cruel and unnecessary animal experimentation, which wastes billions each year and repeatedly creates the pandemics it is supposed to prevent due to how frequently lab leaks occur.

The “war against bird flu” highlights key issues within the pandemic prevention industry, where billions have now been spent killing over 100 million birds, yet all that has accomplished is raising egg prices.

This article explores how many forgotten therapies can treat both severe viral illnesses and rapidly address common conditions like colds and flus.

Almost every year, it seems a pandemic is hyped up. I would argue that’s because:

•They give federal agencies (e.g., the CDC) a way to justify their necessity and get Congressional funding.

•The media thrives off of hooking the public through fear and appeasing its sponsors (e.g., the pharmaceutical industry).

•It sustains a biodefense industry that uses fear to get a lot of money (e.g., 27.7 billion dollars in 2023) to “prevent” pandemics.

•Tackling many of the real health issues facing our country requires confronting the vested interests responsible for them and addressing the underlying causes of chronic illnesses in the country. In contrast, going to war against a disease is far easier and receives minimal pushback but allows the government to present the facade of safeguarding our health.

As such, we will frequently see a myriad of dubious pandemic preventatives be pushed on us (e.g., the mass slaughter of livestock, the newest “emergency” vaccine, or ineffective and unsafe antivirals like Tamiflu). However despite the pandemic failing to materialize or the preventatives failing to work, no one remembers, and before long the cycle begins anew.

In a previous article, I discussed how the biodefense industry regularly cultivates bioweapons in labs to “protect” us from them. Before COVID-19, this industry had been under great scrutiny as many within the scientific community were worried its risky actions could lead to a catastrophic lab leak. However, once SARS-CoV-2 leaked, the entire scientific establishment chose to double down on this research and label any insinuation lab leaks could occur “a conspiracy theory” or “a danger to science.”

These leaks are alarmingly common and remarkably, the industry has not addressed it, as its funding is contingent on a threat continuing to exist (rather than it being eliminated).

Furthermore, many of these lab leaks are quite consequential such as:

The Cambridge Working Group estimated in 2014 that potentially dangerous lab leaks occur, on average, twice each week in the US alone, and by 2018 this number had risen to an average of four times per week.

Numerous fatal lab leaks involving smallpox and anthrax occurred in the US, UK, and Soviet Union.

Note: a more detailed list of consequential lab leaks can be found here.

Vivisection

One of the major sources of extreme and unnecessary animal cruelty is the animal research industry, which sacrifices over 100 million animals each year, frequently in horrific ways that have no scientific value whatsoever.

Vivisection (first used in 1707) describes the practice of cutting open animals with a central nervous system and has been integral to biomedical science. Since this was quite cruel, divided opinions emerged. One school believed medical science must be objective, rational, and dispassionate so it was unethical to be squeamish or sentimental about hurting conscious animals if that “advanced medical science,” while the other believed there was no ethical justification for knowledge gained from vivisection—highlighting the divide in medicine between doctors being technicians who inflicted “necessary treatments on patients” regardless of the suffering it caused and doctors being compassionate healers who made an effort to connect with their patients and their values.

While vivisection gained prominence in the 1800s, its advocates were so cruel they caused a widespread movement against it to emerge and numerous animal welfare laws to be passed.Nonetheless, vivisection persisted (with many of its medical advocates holding the same contempt towards the “anti-vivisectionists” as we see now directed at “anti-vaxxers”) and the opposition to it has become a forgotten chapter in our history.

This in turn touches upon one of the most important points those activists raised—many of the cruel (and often unnecessary) practices in modern medicine arose from the mentality that gave rise to vivisection, so a good case can be made it is in our own interest to eliminate this malignant foundation modern medicine rests upon.

Dangerous and Wasteful Spending

Following the COVID-19 lab leak, the White Coat Waste Project (WCW) discovered an effective way to stop vivisectionist practices by highlighting not only the cruelty involved but also how much money was being wasted on that risky research. As a result, WCW has repeatedly gotten many stories to go viral (e.g., Fauci spending millions on studies where beagles were restrained so they could be eaten alive by sandflies).

WCW’s work touches on a key point—the primary reason much of this research occurs is so that everyone can feed off the grants for it, not because it offers any value to society. For example I recently covered:

•A Colorado University constructing a bat lab to study dangerous infectious diseases which has been widely protested by the community (as they do not want a Wuhan in their backdoor—particularly since FOIA documents showed accidents happened there one to three times a month). However, since that University has received 393 million dollars from the NIH since 2014 and a 6.7 million dollar NIH grant for the lab, Colorado’s government has shut down all attempts to stop the lab.

Fortunately, now that D.O.G.E. is auditing the U.S. government’s spending, many of these wasteful (or fraudulent) grants are being exposed, and it is quite likely this dangerous research will greatly decrease (particularly since the NIH just stopped sponsoring Universities from being able to pocket most of the funding for themselves).

Pumping and Dumping Vaccines

The annual flu vaccines have a rather poor track record as:

The rest of the article is here: https://www.midwesterndoctor.com/p/unmasking-the-great-avian-influenza?publication_id=748806&post_id=158363078&isFreemail=true&r=19iztd&triedRedirect=true&utm_source=substack&utm_medium=email

Once again things are turning and churning.It is as though the wheel has been turned and a new combinations coming up. This once includes more weather ‘anomalies’ along with more physical symptoms.It is well to consider the response of the body to ehe environment — both physical and energetic – before getting panicky about things happening within.You must remember that the body aligns with the environment, ii is physical, and it is motivated by the spiritual and the mental.Now know the there is much power in the mental that can overwhelm the spiritual and the physical not because it is necessary stronger, but because of the attention that is being placed in t hat arena. So, when you feel yourself being drawn into a strong consideration of what is going on in the body, it is well to sit back and see whether that consideration is a distraction or whether it is the body going into survival mode.As a distraction what is happening is that there is an outside force at work on you and perhaps the whole of the humanity —- we thought to say ‘the physical’ because in most cases it is dealing with all the people in the physical world, and in fact, it can also be affecting the natural world, however in order to make things clearer and to bring focus back to the physicality we chose the other word, ‘physical;’.

The physical as you know is but once facet of the individual and not necessary always the most…. Effective or…….. we are looking for a word and we cannot at this moment find it n your vocabulary however the physical has its place, but the determiner of the body is a team.You need all the various elements, but at one time one element takes over and at another (time) a different one.However the importance in this level, in this dimension is for the body to continue on, and therefore one thinks mainly of the physical, but as you have seen in spiritual….. and energetic healing, what can be done is that a new alignment of the physical can be achieved through dealing with the energy body. This body’s one of the layers of the person, can change the physicality if , and of course, this is is important, if it is so allowed for the physical motivator always is watching what is going on and at times will override what is best for the totality of the body/bodies.

We know this is off the subject a bit, but allow its to make an analogy with the weather.When the environment, particularly the weather is being manipulated, then the alignment of the various areas of the environment is out of whack, and there can be extreme events that were not actually part o the real motivation of the weather.These things can be caused by the atmospheric heaters that are in action all over the world.As we have mentioned earlier, they have reached a point, a tipping point, at which these technological means will be thwarted by the earth, yes, but also by the actions of these terrible individuals.They will be thwarted because things are so out of balance that they are toppling and can no longer be righted by technological means, so look for unexpected, (???) unexpected, (parts) of the earth to work towards righting the imbalance.Know that this alway will (affect) humankind.It is well to look for alternative remedies and keep them close at hand for they posses an energetic component that can help the body respond to the rocking and rolling..